Plastics & Consumables, Alfen

Small Cap Earnings Review 26/08/22

Skan Group AG - 1387m CHF

I get excited when I hear the word “consumables” coming out of a MedTech presentation. Let me explain:

Once a costumer buys a machine, they have a long term (>8 years) need for spare parts, consumables & services, which they can only purchase from the same company.

Think about the number of times pharma researchers have to put vials inside machines. That adds up to a lot of high margin revenue.

This is precisely the image I pictured when researching Skan Group.

They are in the business of selling high-end isolators used for pharma R&D, and provide the consumables & services that go with it. In fact, they are the number one player in the high-end of the market & are looking to increase their share of the lower end.

Net Sales were up 18% in H1 22 with an EBITDA margin of 9%. More importantly, the order backlog stands at 263m CHF a 68% increase year-over-year.

Skan also made the acquisition of Asceptic Technologies, which developed the ‘AT-Closed Vial Technology’. Skan’s customers are going to need a lot of premium vials to make good use of the isolators, and this acquisition strategically ensures they can attend to their customers’ needs.

The isolator market is expected to grow ~10% per year. Since Skan is a leader, it will probably outperform. Thus, double digit sales growth & operating leverage driven by consumables is in the cards.

For now, I believe the valuation is a bit rich (~40x FY22 EV/EBITDA), but I may be wrong. Anyways, I’ll be following it closely.

Alfen NV - 2487m €

The stock goes up yet the valuation gets cheaper. Not many stocks are like that !

Alfen’s print was nothing short of an absolute blowout, lifting revenue guidance from 380m€ to 440m€ at the midpoint.

The Dandy did expect this. We were forecasting 422m€ back in May when consensus was still at 350m€. Our thesis was that Alfen would continue to gain market share in the short term as their unprofitable competitors struggled with supply chain and cash management. It definitely played out. We estimate that Alfen gained 5-10% market share in Q2 alone and has 30-40% market share in Europe for EV charging.

If you’re interested, you can find the May article on Alfen below:

The valuation seems very reasonable now (30x EV/FY22 EBIT), however the main reason we didn’t invest in Alfen, and will still be waiting to invest is that their is no news of a capacity increase.

We expect Alfen will produce ~290k chargers this year. Extrapolating their current market share to 2023, assuming 20% growth in EVs and a corresponding 90% increase in EV charging production (see Alfen article to understand assumptions), Alfen would produce more than their current ~450k annual capacity. Therefore, we would like to see them 5x capacity again.

Given management’s tone, they seem to expect to lose market share and/or the market to cool down starting in H2 22. Thus, our forecasts could be way off, and growth could be something like 25-30% instead of 90%.

An increase in capacity before the end of the year would help reduce the uncertainty. They will eventually need it, so its not really about if, its about when, the earlier the more bullish. It took them a few months back in 2019-2020 to add an extra 360,000 EV charging points per year worth of capacity.

SP Group: 3340m DKK

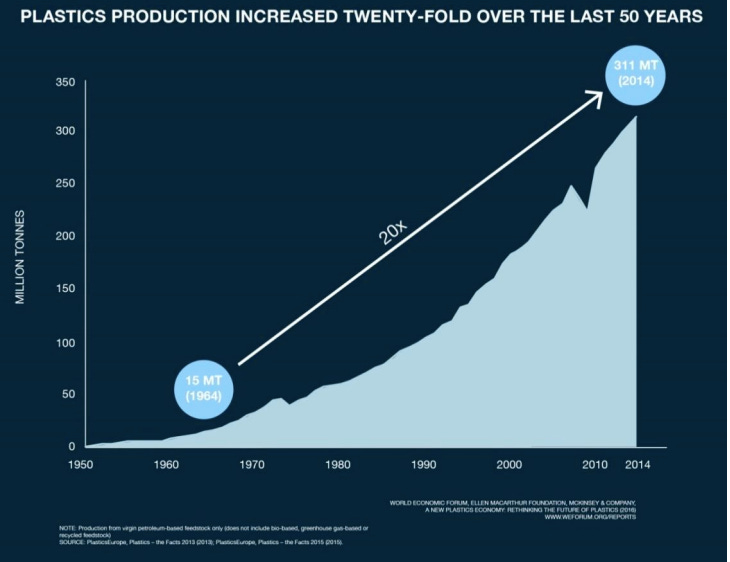

You may or may not be surprised to hear that plastics have been a growth market for the past 50 years:

But when you think about it, everything around you requires plastic to some extent: cars, computers, water bottles… you name it !

So if you think GDP is going to grow, and people around the world are going to keep on buying more stuff, well stocks that make plastic components such as SP Group A/S aren’t a bad place to be looking for growth.

By growth, I mean 5-6% organic revenue growth per year on average.

But that’s not all: Businesses such as SP Group (we could also mention NOLATO AB) benefit from two underlying return tailwinds on top of the decent market growth:

Their customers want to concentrate their supplier base into a few trusted suppliers, because they want to be able to ensure high quality (especially if the end market is medical) and timeliness. Therefore, larger, established players naturally gain market share.

Nobody really cares about plastic companies, so they are able to make very attractive acquisitions at 4-6x EBIT, improve the cost base and use their distribution network to grow the business.

When you add all of this up, you get the 18.6% EBITDA growth SP Group saw in H1. And this isn’t a fluke, this growth has been going on for quite a few years now:

SP Group’s ambition is to grow its EBIT at a 20% CAGR over the next 2.5 years, which would put it at ~9x EV/FY24 EBIT. Historical multiples at a constant leverage ratio imply 50% upside on a 2.5 years basis.

Skan: If they are no1 in the market and have so much repeat business, how come they barely make money: 2020: 4m CHF 2% margin, 2021: 10m 4% margin, All that for a company with 1.3bn mcap.