Long Semi Equipment/Short Chipmakers

Industry Deep Dive #1

Introduction

Lately, the topic of semiconductors has been discussed a lot. The shortage we experienced in 2021 made people realise just how crucial they are to any kind of hardware, however sophisticated it may be.

Now, you might think that you should invest in good semiconductor stocks, as they are extremely important right ? Well, that may work, however, semiconductors are a depreciating commodity, as customers only care about performance and price. Furthermore, competition is harsh and product cycles are quick. It is certainly not a very attractive industry, and a leader like NVDIA/AMD could quickly end up behind, leaving you holding a bag that you paid 60x earnings for.

However, the semiconductor equipment market does not obey the same rules.

Semiconductors continuously push back the law of physics. So, imagine how hard it must be to make the machines that make semiconductors. Hard to the power of hard is the answer.

In my first industry deep dive, I will look at the different players in this space, and I will explain who does what and the whole process in detail, in order for you the reader to understand where to put your money.

A quick overview of the semiconductor market first

Chips

The semiconductor market is roughly worth 800b USD. It is dividable into three types of chips:

Silicon: Represent 600b USD. These are what we typically call semi-conductors. They are broadly three types of chips supplied here:

Microprocessors, for smartphones, PCs and Tablets

Memories, (DRAM etc)

Analog chips: Smartphone, Automotive, Industrial ( the “dumb” chips)

Glass: Represents over 150b. More tilted towards sensors and medical, but very broad as well.

Compound Substrate: LED, LIDAR etc… Basically for lighting or power inverters for instance

Chip makers

IDMs: Intel & Samsung, who control the whole production process

Process specialised companies

Fabless: Qualcom, Broadcom etc… They focus purely on the design

Foundries: TSMC, UMC etc… They only produce the chips

IP: ARM, Rambus… They only focus on circuits, system design and sell to the chipmakers

As production needs high capex, foundries have a competitive advantage due to the replacement cost and economies of scale. Therefore, the market is moving towards a highly specialised supply chain and IDMs find it harder to compete.

How do you make a semiconductor ?

It Starts With A Wafer

This is basically the semiconductor equivalent of a blank page. Companies like Siltronics specialise in making those things, but they are even more commoditised than chips are, so this subpart of the industry won’t be discussed here.

The Front End Process

The front end process is where all the magic happens, and is the most technical part of all. It represents over 75% of the cost of making a chip. I am not going to go into the details of this process, as it is highly technical. I’ll just give you the overview.

There are grosso modo 3 things you need to do to a wafer before it turns into a bunch of chips:

Lithography: The semiconductor equivalent of painting. A photo-sensitive material is applied to the wafer, “photo resist”, and is used to design circuits. This typically accounts for >30% of the cost of semiconductor manufacturing.

Etch: This is the process of cleaning a wafer, removing unnecessary parts to create the desired pattern.

Deposition: The process of stacking different layers on top of each other

Basically, the process is a repetition of these 3 steps. There are other steps such as stripping, cleaning and implantation, but they make up less than 25% of the process. The three above are the ones we should know about in order to make money.

Finally, Back-End

The back-end process is basically process control and yield management. This is about optimising your bang for buck in the production process.

Who does what ?

For these processes, you need machines, typically referred to as “Semiconductor Equipment”. The capex involved in creating the factories that make these machines is on a whole other level.Furthermore, it is an incredibly hard task that requires a lot of know-how.

Therefore, companies that become experts at making equipment that enable one part of the process tend to win the whole market. Also, they become of strategic importance to their country of origin.

I will now discuss the key players in each different segment.

Front-End equipment makers (80-90B USD market)

#AMAT

Applied Materials has market share in all of the equipment types except Lithography. Its speciality, however, is in deposition, where it retains about half of the market, worth around 14B USD. It has 18% in Etch and 12% of the back-end market.

#ASML

ASML is the clear winner in the wafer exposure sub-segment of Lithography. This market is worth about $14B and ASML has over 80% market share. It is by far the most important company on this list.

#LAM

Lam Research Coporation has about 40% of the market in the Etch category, worth around $20B.

#TEL

Tokyo Electron Limited is the dominant player in wafer cleaning/photo-resist which is worth about 5b , and holds around 90% market share. This is basically the part of Lithography that ASML does not cover. It also holds a strong market share in Etch (20%) and Deposition (11%)

Backend 15B USD market

#KLA

KLA Corporation is the key player in the back-end solutions. It has over 50% of the market.

Why the equipment makers ?

Semiconductor capex is expected to rise, due to increased demand for the end-product and geopolitical reasons. I won’t go into detail about why semi-conductor demand is expected to rise, because that’s beyond the scope of this article, however, what is more interesting to us is the geopolitical turn.

The 2021 shortage has brought about concerns of supply availability in times of crisis. The world realised two things:

Semi-conductors are essential

The global supply chain cannot be relied on in times of crisis

Achieving chip self-sufficiency suddenly became a matter of national security, and states are reacting:

France decided it wants to make its own chips

TSMC is planning to build a plant in the US in case China invades Taiwan

Intel announced a multi-billion capex plan.

Now, if we add 2+2, this means two things:

The world is going to get flooded with chip supply, and competition will increase

Equipment manufacturers are going to have 10 year backlogs

This is why you want to be long the equipment manufacturers, and avoid the chip makers.

Financials

The equipment manufacturing market is expected to grow at a double digit rate in the medium term, with two segments growing slightly faster: Backend & Lithography. This contrasts well with the expected growth in chips of high-single digits.

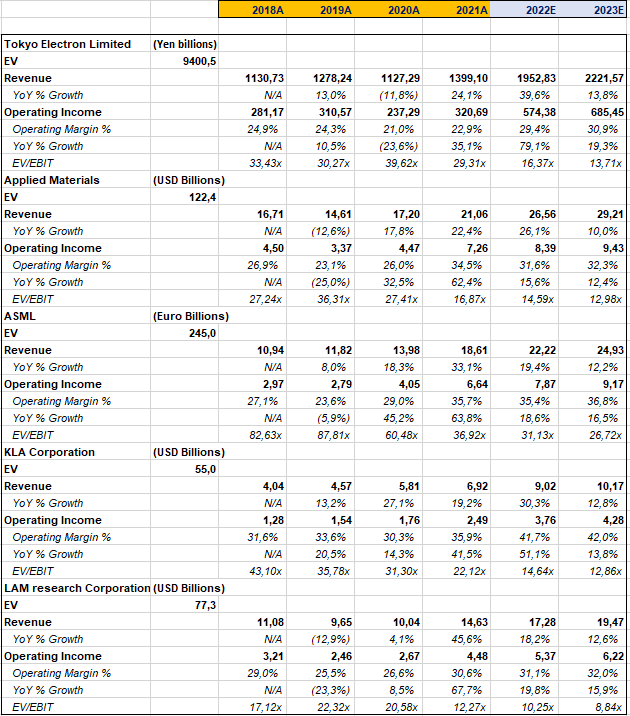

Overview of the key players

Thoughts and picks

As I said, all those companies have the same driver and have enormous staying power, so you could theoretically just buy an equal weighted basket of them to play the theme.

However, I like AMAT the least, as it has its activities spread out into multiple segments, of which only one it dominates, but not by much.

Furthermore, though ASML has arguably the strongest moat in this list, it is twice as expensive.

Then, LAM only has a slightly dominant place in the etching equipment market, competing with AMAT and Tokyo Electron.

This leaves KLA corporation, the leader in back-end solutions, which I think is the most overlooked segment by investors. This is my top pick, and it is also in the fastest growing segment by far.

I also think Tokyo Electron is a good pick, as it has the strongest market share in its major segment (wafer cleaning/Photo resist), which also brings a lot of bargaining power when competing in the etching segment.

Summary

I believe that there are much more barriers to entry and competitive advantages in the equipment makers compared to semiconductor design and manufacturing. They will grow faster than the manufacturers, and they have much more staying power.

I do not own any of the companies above right now, but may initiate a position in the future. This is not financial advice.